Venture capital is a hell of a drug. Used properly, it’s like adrenaline energizing many of the greatest companies of the past fifty years. Used incorrectly, it creates toxic dependencies.

The conventional wisdom in the startup community is that when building the very best companies, more capital can be leveraged to accelerate even greater growth. But does this “go big or go home” approach stand up to scrutiny? In the best case scenarios, do companies that load up on venture capital actually outperform those that more efficiently deploy capital? We looked at 71 tech IPOs from the last five years to find out.

Efficient entrepreneurship

At Founder Collective we’ve been talking to our community about the virtues of what we call “efficient entrepreneurship.” We’ve written recently about the downsides of heavily funded companies, including the loss of exit optionality, and perils of unsustainable burn rates, but how does aggressive venture capitalization look on the upside? By studying the best cases of venture capital success, what can we learn about the benefits of raising lots of money?

The results were surprising – by examining the technology IPOs of the past five years, we found that the enriched (well capitalized) companies do not meaningfully outperform their efficient (lightly capitalized) peers up to the IPO event and actually underperform after the IPO.

Raising a huge sum of money is a requirement to join the unicorn herd, but a close look at the best outcomes in the technology industry suggests that a well-stocked war chest doesn’t have correlation with success.

Of the 20 most successful publicly-traded startups over the past five years (measured by current market cap), 14 raised in the neighborhood of $100M or less. Six raised less than $50M. One raised no capital at all. These are shockingly small amounts of money when you consider the median privately-funded unicorn has raised $284 million dollars.

Methodology

Evaluating startup performance is a messy business. Late stage companies are rightfully secretive. Acquisitions are messy financial affairs often engineered to obfuscate the true value of a transaction. The IPO market was the most transparent proxy we could find, and while imperfect, it is instructive. With notable exceptions, most of the biggest outcomes in venture capital are a result of IPOs. By studying the relationship between venture capital and IPOs of the past five years, we can get an idea of whether raising more capital in the best companies correlates to better outcomes.

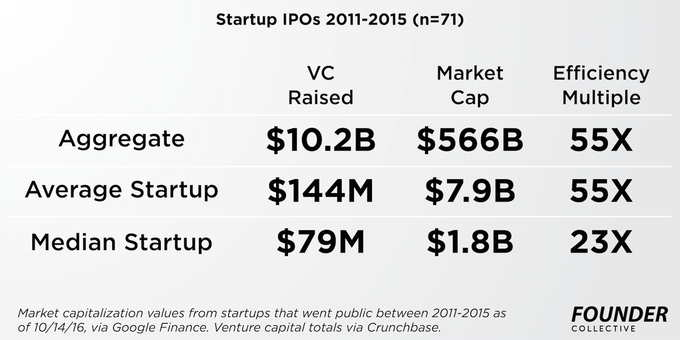

The data

-

The data includes 71 companies that raised a total of $10.2B in venture capital

-

Their combined market cap is $589B, or 57X the capital invested

-

The average startup on the list raised $144M in VC to build a company worth $8.3B

-

The median startup on the list raised $79M in VC to build a company worth $2.0B

Pretty exciting results overall! Of course this data set reflects nearly all of the best outcomes in the venture industry over the last five years.

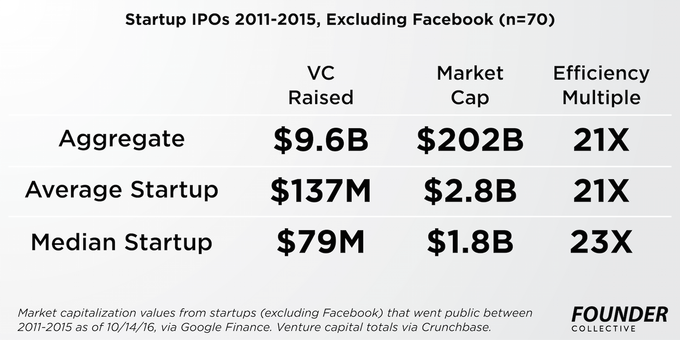

Setting Facebook Aside

Acknowledging that there is only one Facebook and that it is an extreme outlier among outliers, we excluded the company from most of our analyses. Absent Facebook, the overall numbers still look pretty strong, but it is astounding to see how much one company skews the totals:

-

70 companies that raised $9.6B in venture capital

-

Their combined market cap is $217B, or 23X the original investment

-

The average startup raised $137M to build a company worth $3.1B

-

The median startup on the list raised $79M in VC to build a company worth $1.9B

Exclusions

We only looked at companies that held IPOs between 2011-2015. It would be interesting to go back further than five years, but it is also instructive to examine what is effectively the “unicorn era” in which private companies raised unprecedented amounts of capital. We excluded companies that were founded prior to 2000 (e.g. GoDaddy, FirstData), companies with unorthodox financing paths (e.g. Match Group, RetailMeNot), and companies in Asia and Russia, because they have significantly different financing environments. The result is a dataset, available for review, that includes 71 companies. Most of the data was taken from Crunchbase, except where noted.

We also excluded late-stage private equity, secondary offerings, and debt from the calculations, though they are recorded in the spreadsheet. We were less interested in the money raised in the IPO, as we viewed as a graduation point from the venture capital game and is largely a direct function of company size. The data certainly contains imperfections, though we did our best to get it right, and we’re open to feedback on the dataset, which is why we’re making it public.

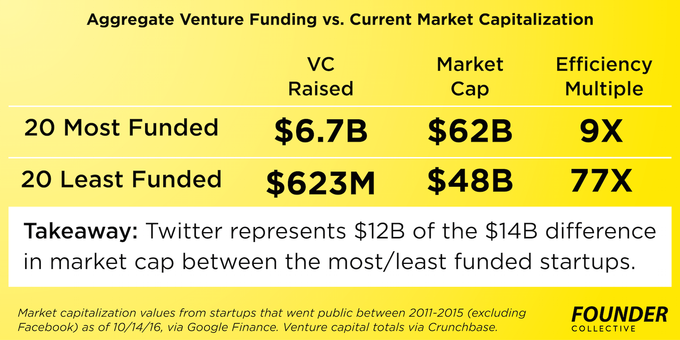

The best case for “Big VC”

This data might suggest that “go big or go home” makes some financial sense, especially for investors. The most heavily funded companies do have larger total dollar returns. Counted together, the 20 best funded companies on the list raised $6.7B in VC and have an aggregate market cap of $69B, for a ~10X return.

The 20 least funded companies on this list only raised $609M in VC, yet managed to return $51B to investors, or an 84X return.

That’s a $18B dollar difference in aggregate returns. That’s non-trivial, especially to VC as an asset class. However, ~$16B of that difference is accounted for by Twitter, who raised a little less than a billion dollars in VC. So aside from those Facebook and Twitter, venture capitalists spent ~$5B to make an incremental $2B. It’s important to note that the stock market is volatile and that over the course of writing this post, the 20 most enriched companies have fluctuated dramatically. Still, the variance is usually driven by one or two outlier companies.

It is true that there are a few companies founded each year that drive the bulk of the returns. It is also true that in the case of only a couple of outliers (Facebook and Twitter), heavily funding the best companies is a winning strategy for investors. However, It is not clear that VCs have been able to consistently identify the best performers and have instead overfunded even the most successful companies.

This isn’t a knock on the VC model—it’s an asset class predicated on risk. The best firms in our industry have shown an ability to run this high risk playbook over many funds.

It should be a lesson for founders though. Companies like Facebook and Twitter are critical for the health of the ecosystem, but are not a good model for other startups. Unless a founder is very confident that they are building the next Facebook scale business, they would be better served focusing on creating higher multiples instead of a higher exit value.

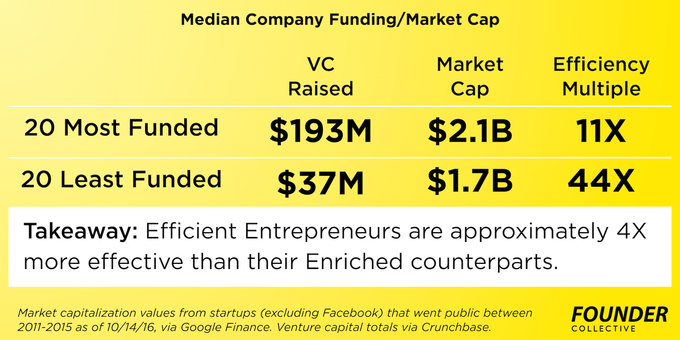

VCs have a portfolio, entrepreneurs get one shot (at a time)

VC can afford to risk overfunding a dozen companies in order to be a part of the epoch-defining winners, but entrepreneurs only have one shot. As a founder, are you willing to take 5X more risk for what, even in the best cases, results in a 15% premium? That’s basically what the companies on the top of this this list did:

The financial calculus for founders is even worse than it appears. Incremental funding will probably come with extra dilution, and pre-IPO preferences that will favor the VCs if the startup’s hot streak falters and it doesn’t get public. Beyond the magnitude or risk, more capital limits the number of possible exit paths. The founders of 20 most efficient companies likely could have successfully sold their companies at any point along their development for a healthy return. Their enriched counterparts are locked into billion dollar exits with diminishing returns on capital.

Is this actually the best model for VCs?

It’s conventional wisdom in the VC market that investors should heavily lean into their winners, but are you better off doubling down on winners for diminishing returns or funding a new crop of startups with the potential to return 10, 20, or 30X?

Davids versus Goliaths

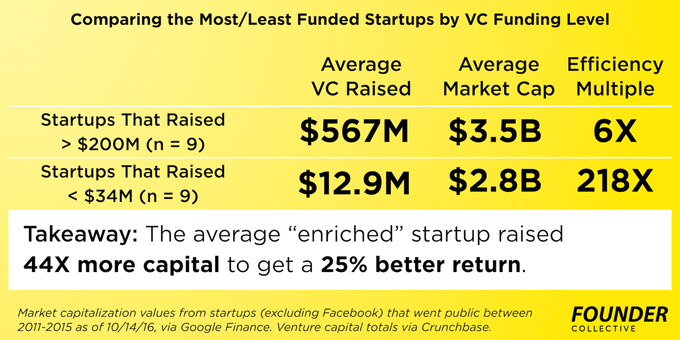

Though it’s a ridiculously small sample, look at companies that raised an objectively large sum of money—say over $200M (nine companies in this sample), versus an equal number at the bottom of the list. The results are staggering:

-

The most enriched companies raised $567M to return $4.2B or 7X

-

The most efficient companies raised $11.3M to return $3.0B or 264X

-

The most enriched companies raised 49X more money to get a 42% better return

Power laws in venture capital are real, but fundraising is a poor predictor of them. A couple of great companies raised a lot of money, but more money doesn’t make runaway successes any more likely. If you exclude Twitter as well as Facebook, the top 10 most efficient startups actually outperform the 10 most enriched companies.

Less money = better companies?

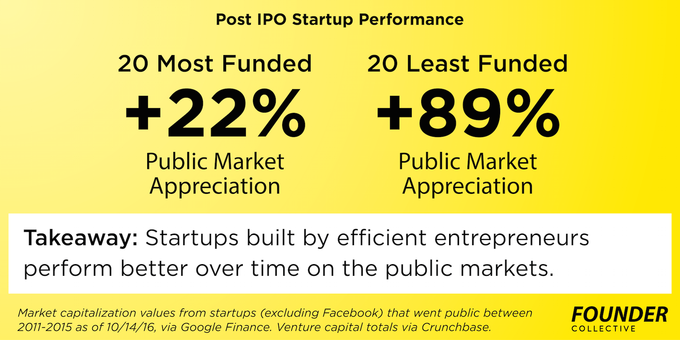

Market value at the IPO is important because it is often a marker of the venture capital exit value, but it’s also interesting to consider how these enriched companies compare to their efficient peers in the long term as public companies. Does instilling a sense of fiscal restraint early, where growth comes from disciplined customer acquisition, not a venture capitalist’s checkbook, lead to more sustainable businesses?

It turns out the efficient companies have performed significantly better as public companies than the enriched group:

This trend is even more startling from a modal perspective:

Our hypothesis is that too much capital over time creates a culture that substitutes cash for creativity and operational discipline. Big balance sheets allow companies to grow inefficiently, to paper over problems with headcount and spend, rather than confronting the core engine of value creation. Having less money forces a management team to make hard decisions early on and to cut off potentially wasteful problems that otherwise could linger indefinitely. This efficient ethos becomes part of the long term culture of…