The delivery and progress of monetary know-how developed largely over the past ten years.

So as we glance forward, what does the subsequent decade have in retailer? I consider we’re beginning to see early indicators: within the subsequent ten years, fintech will turn into transportable and ubiquitous because it strikes to the background and centralizes into one place the place our cash is managed for us.

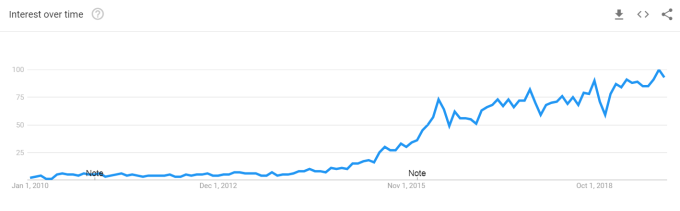

When I began working in fintech in 2012, I had hassle monitoring aggressive search phrases as a result of nobody knew what our sector was referred to as. The best-known corporations within the house have been Paypal and Mint.

Google search quantity for “fintech,” 2000 – current.

Fintech has since turn into a family title, a shift that got here with with prodigious progress in funding: from $2 billion in 2010 to over $50 billion in enterprise capital in 2018 (and on-pace for $30 billion+ this 12 months).

Predictions have been made alongside the way in which with combined outcomes — banks will exit of enterprise, banks will catch again up. Big tech will get into shopper finance. Narrow service suppliers will unbundle all of shopper finance. Banks and massive fintechs will gobble up startups and consolidate the sector. Startups will every turn into their very own banks. The fintech ‘bubble’ will burst.

https://techcrunch.com/2019/12/22/who-will-the-winners-be-in-the-future-of-fintech/

Here’s what did occur: fintechs have been (and nonetheless are) closely verticalized, recreating the offline branches of monetary companies by bringing them on-line and introducing efficiencies. The subsequent decade will look very completely different. Early indicators are starting to emerge from ignored areas which counsel that monetary companies within the subsequent decade will:

- Be transportable and interoperable: Like cellphones, prospects will have the ability to simply transition between ‘carriers’.

- Become extra ubiquitous and accessible: Basic monetary merchandise will turn into a commodity and convey unbanked contributors ‘online’.

- Move to the background: The customers of monetary instruments gained’t must develop 1:1 relationships with the suppliers of these instruments.

- Centralize into a number of locations and steer on ‘autopilot’.

Prediction 1: The open knowledge layer

Thesis: Data can be brazenly transportable and can now not be a aggressive moat for fintechs.

Personal knowledge has by no means had a second within the highlight fairly like 2019. The Cambridge Analytica scandal and the information breach that compromised 145 million Equifax accounts sparked at the moment’s public consciousness across the significance of information safety. Last month, the House of Representatives’ Fintech Task Force met to judge monetary knowledge requirements and the Senate launched the Consumer Online Privacy Rights Act.

A drained cliché in tech at the moment is that “data is the new oil.” Other issues being equal, one would count on banks to take advantage of their data-rich benefit to construct one of the best fintech. But whereas it’s obligatory, knowledge alone shouldn’t be a ample aggressive moat: nice tech corporations should interpret, perceive and construct customer-centric merchandise that leverage their knowledge.

Why will this transformation within the subsequent decade? Because the partitions round siloed buyer knowledge in monetary companies are coming down. This is opening the taking part in area for upstart fintech innovators to compete with billion-dollar banks, and it’s taking place at the moment.

Much of that is because of a comparatively obscure piece of laws in Europe, PSD2. Think of it as GDPR for cost knowledge. The UK grew to become the primary to implement PSD2 coverage underneath its Open Banking regime in 2018. The coverage requires all giant banks to make shopper knowledge accessible to any fintech which the buyer permissions. So if I preserve my financial savings with Bank A however need to leverage them to underwrite a mortgage with Fintech B, as a shopper I can now leverage my very own knowledge to entry extra merchandise.

Consortia like FDATA are radically altering attitudes in direction of open banking and gaining international help. In the U.S., 5 federal monetary regulators lately got here along with a uncommon joint assertion on the advantages of other knowledge,…